How Higher Gas Prices Impact Your Wallet and Your Investments

For most Americans, the price of gasoline at the pump is one of the most visible ways the conflict in Iran touches their daily lives. Gas prices are hard to miss — they are posted on large signs and updated often. Filling up the tank at least once a week is a necessity for getting to work, school, and the grocery store. Diesel prices matter just as much, since they affect the cost of transporting and making goods throughout the economy. This is why fuel prices are closely watched as economic signals, and why the ongoing situation in the Middle East has become a growing concern for everyday consumers and investors alike.

As the conflict enters its second month — with news swinging between potential peace talks and possible escalation on a daily basis — oil prices have stayed high with big swings throughout each trading day. Brent crude (a global benchmark for oil prices) is now trading above $110 per barrel, and WTI (a U.S. benchmark) is above $100. These elevated energy prices are expected to affect household budgets, inflation (the general rise in prices over time), and decisions made by the Federal Reserve (the U.S. central bank that manages interest rates).

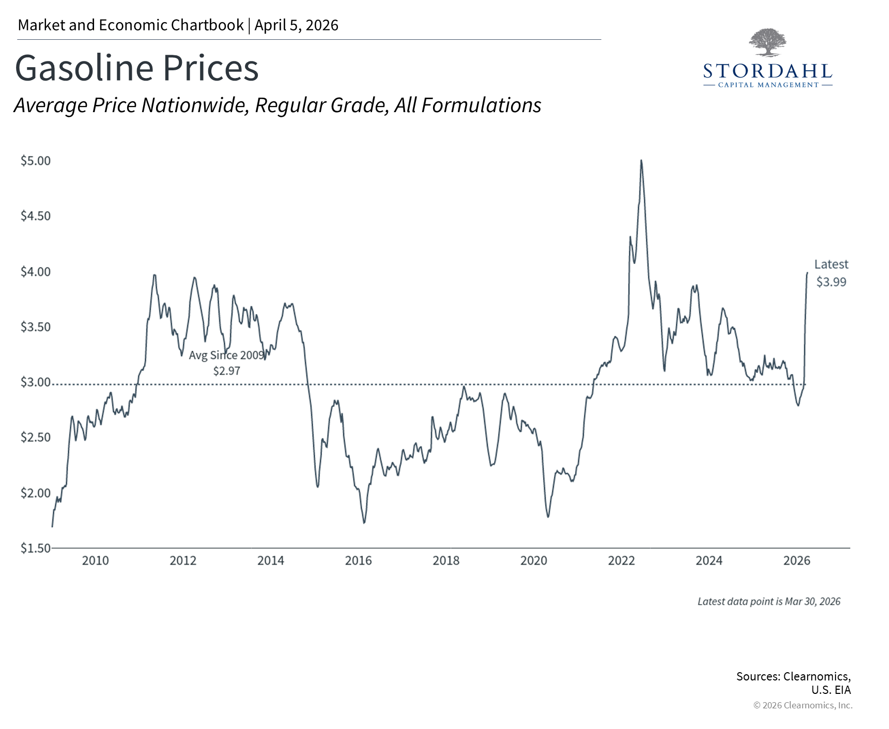

Gasoline prices have risen sharply

The national average price for regular unleaded gasoline has climbed to around $4.00 per gallon — an increase of more than a dollar per gallon in just one month. While this is still below the record high of $5.00 per gallon reached in 2022, prices could rise further if oil remains expensive. For most households, buying gasoline is not optional. Even if people drive a little less, higher gas prices will cut into the money families have left over for other spending and saving. And even though electric vehicles are becoming more popular, most cars on the road today still run on gasoline, so nearly every household feels the impact.

The effect of higher gasoline prices on consumers is both direct and indirect. A simple calculation shows how the current price increase affects everyday spending. If the average fill-up is 15 gallons, then the recent price increase adds $15 to each gas station visit. For someone who fills up once a week, that adds up to roughly $780 less per year.

For someone earning the federal minimum wage of $7.25 per hour, that would mean working more than two extra hours just to cover the added gas cost. The impact looks different for higher earners. The typical American household earns just over $70,000 per year after taxes, according to the latest Census Bureau statistics, meaning the extra gas cost represents just above 1% of their after-tax income. While this leaves less money for other purchases or savings, most households at this income level can likely manage without serious financial hardship.

In this way, higher gasoline prices act like an added cost that comes directly out of consumers’ pockets. While it is important not to downplay the difficulty this creates for some families, most households will likely be able to get through this period.

From an investing perspective, the broader economic drag can add up quickly. When you multiply the extra spending across millions of households week after week, the total effect on consumer spending and savings can become significant if oil prices stay high for a long time. But the indirect effects may be even more important. Gasoline and diesel are used in almost every part of the economy — transportation, manufacturing, farming, and delivery all rely on fuel. That means higher fuel costs push up the price of a wide range of goods and services. This is why oil price increases do not just affect energy bills — their effects spread throughout the entire economy over time.

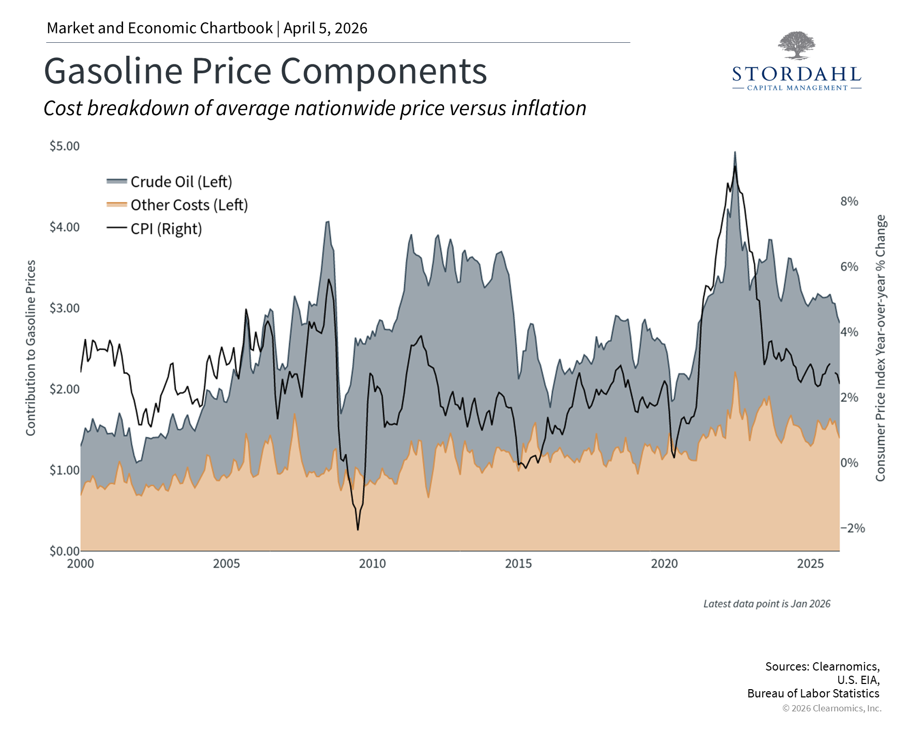

Gasoline prices are not just about oil

Knowing what actually determines the price of gasoline can help put the current situation in context. According to the U.S. Energy Information Agency, roughly half of what you pay at the pump reflects the cost of crude oil itself. The other half is made up of refining costs (turning crude oil into gasoline), transportation and distribution to gas stations, sales and marketing expenses, and federal and state taxes.

These additional costs also help explain why people in some states pay significantly more than the national average for gasoline. The accompanying chart, based on the latest available data — which does not yet reflect the most recent price jump — shows how these different components have changed over time.

This breakdown also helps explain why gas prices do not rise or fall in perfect step with oil prices. It also takes time for changes in oil market prices — which can shift quickly in the futures market (where buyers and sellers agree on prices for future delivery) — to show up at the pump. The chart also highlights the annual change in the overall Consumer Price Index (a measure of inflation) and its clear connection to oil prices over time.

For investors, it is also worth noting that the oil futures market is currently in a state called "backwardation." This means that oil prices today are much higher than what traders expect them to be in the future — a notable shift from just a month ago, when future and current prices were roughly the same. In other words, while today’s prices reflect the current disruption in the Middle East, traders are signaling they expect oil prices to eventually come back down once the situation stabilizes. This does not guarantee a quick resolution and can change as new information emerges, but it does suggest that markets see the current price spike as a temporary shock rather than a lasting change.

Higher energy prices complicate the inflation picture

For investors, energy prices directly affect headline inflation — the broadest measure of rising prices that includes food and energy costs. After several years of improvement in energy-related inflation readings, the recent jump in oil and gasoline prices will almost certainly push headline inflation higher in the months ahead. Organizations such as the OECD (an international economic research group) now estimate that U.S. inflation could rise faster than expected this year.

This matters for a few reasons. First, consumers are still recovering from the surge in prices that followed the pandemic. Second, both stocks and bonds have historically struggled when inflation rises unexpectedly, since it increases costs for companies and reduces the purchasing power of fixed payments from bonds. That said, markets have shown considerable resilience over the past several years, even during difficult inflationary periods.

Third, and perhaps most relevant for financial markets right now, rising inflation makes the Federal Reserve’s decisions more complicated. The Federal Reserve adjusts interest rates to help manage inflation and economic growth. Markets have already shifted their expectations, with traders now assigning a greater probability to the Fed holding rates steady or even raising them rather than cutting. This change in expectations has added uncertainty for both stock and bond markets, especially as the Fed undergoes a leadership transition in mid-May.

Economists generally view these types of disruptions — where prices rise because of a reduction in supply rather than increased demand — as temporary. This does not necessarily mean high oil prices will be short-lived, but it does reflect the idea that prices should ease once supply comes back online.

While the current situation is still challenging for consumers, it is quite different from the 1970s energy crisis. Notably, the U.S. is now the world’s largest oil and natural gas producer, and the Federal Reserve has a much stronger track record of keeping inflation expectations under control. This makes today’s economic and financial market environment more stable than it was in the past. For investors, the best approach continues to be staying invested with a well-constructed portfolio and a clear financial plan. This strategy served investors well during the last inflation spike in 2022, and remains the most reliable way to work toward long-term financial goals.

The bottom line? Rising gasoline prices are a burden for consumers and will likely push headline inflation higher. However, history demonstrates that markets and the economy have successfully navigated past energy shocks. Investors should maintain a long-term perspective, avoid overreacting to daily headlines, and stay focused on their financial plans.

Questions? We offer a complimentary 15-minute call to discuss your concerns and explore how we can assist you.

A Weekly Perspective on Planning and Markets

Each week, we share The Week in Review — a short collection of articles on

financial planning and wealth management, along with a brief overview for context.

One email per week. No promotions, no sales – just clarity.

Stordahl Capital Management, Inc is a Registered Investment Adviser. This commentary is solely for informational purposes and reflects the personal opinions, viewpoints, and analyses of Stordahl Capital Management, Inc. and should not be regarded as a description of advisory services or performance returns of any SCM Clients. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Advisory services are only offered to clients or prospective clients where Stordahl Capital Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Stordahl Capital Management unless a client service agreement is in place. Stordahl Capital Management, Inc provides links for your convenience to websites produced by other providers or industry-related material. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third-party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax, or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.