The Week in Review: July 13, 2026

Oil Has Given Back Gains, but Gasoline—Not So Much

Just before the start of the war, WTI crude oil traded at about $67 per barrel, according to MarketWatch. By last week, the price of oil had fallen to within about $1 of its pre-war price.

However, the same can’t be said for the average U.S. price of regular gasoline, which remains over 80 cents per gallon above the late February price, according to GasBuddy. What gives?

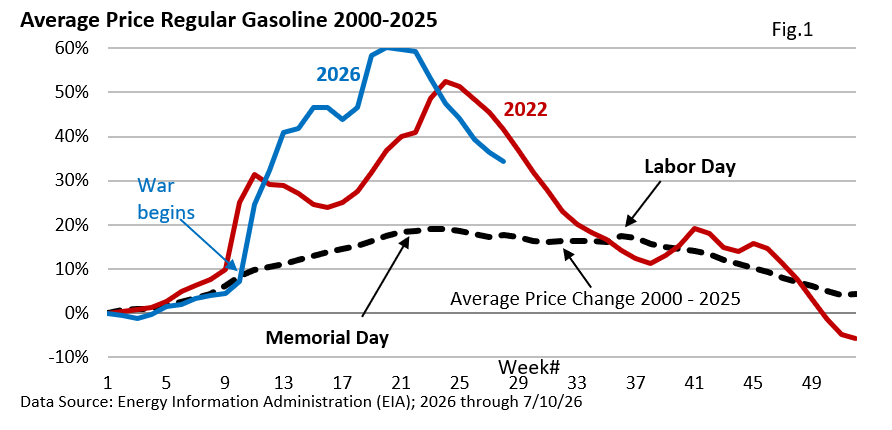

First, seasonality affects gasoline prices. Figure 1 illustrates the average change in gas prices over the last quarter-century. On average, prices rise until Memorial Day, plateau over the summer, and drop after Labor Day.

To begin with, seasonality is a factor. But seasonality isn’t entirely to blame.

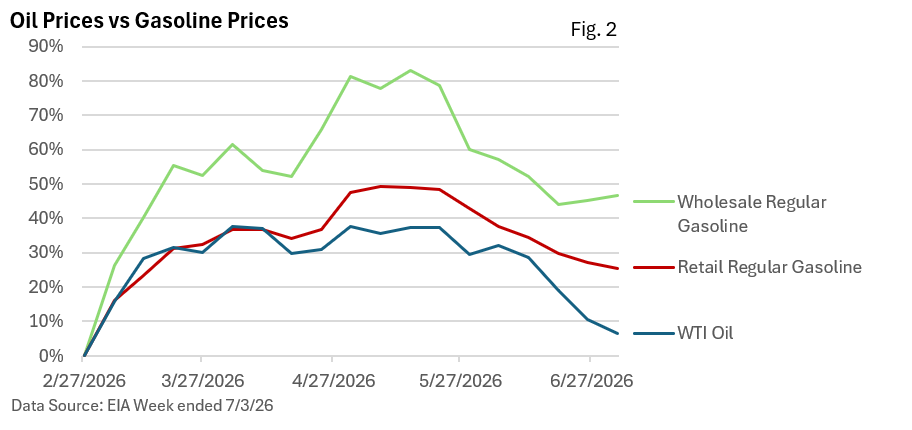

Figure 2 highlights the changes in wholesale gasoline prices, retail gasoline, and WTI crude oil since the beginning of the war—see Figure 2

Oil is nearly back to the pre-war level—not so for gasoline.

Note that wholesale gasoline remains elevated. If wholesale gasoline had decreased in tandem with oil, we could hold retailers and their fatter profit margins accountable. But that doesn’t appear to be the case. Instead, the spread between wholesale gasoline and oil is quite elevated.

So, why have retail and wholesale remained high? Well, there are various factors coming into play.

According to the EIA, refineries have ramped up production of jet fuel and propane. Currently, both jet fuel and propane stockpiles in the U.S. are above the 5-year range for this time of year, even as U.S. exports of these products have surged. But the increase in jet fuel and propane production has come at the expense of gasoline.

According to Bloomberg, gasoline inventories are at a 14-year low for early July.

So, tighter domestic supplies and seasonality are contributing to the slow decline in gasoline prices.

Finally, there’s another dynamic that industry observers often refer to as “rockets and feathers.”

As the name implies, gasoline prices tend to shoot up like a rocket when crude oil prices rise but drift lower like a feather when oil prices decline. That’s not much comfort when filling up at the pump, but it’s a recognized phenomenon in the industry.

If oil prices stay within the current range and traffic from the Middle East resumes (a significant if), consumers may finally experience more substantial relief in the fall.

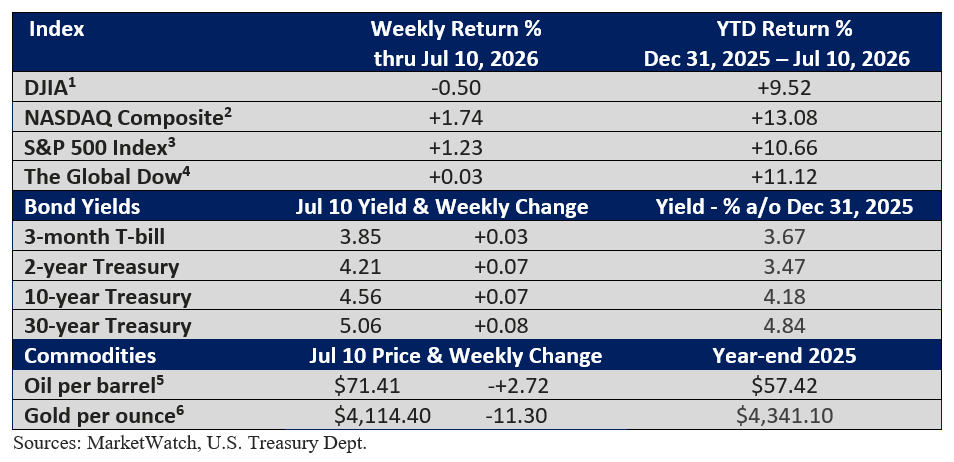

For investors, elevated gasoline prices aren’t being reflected in stock prices, with the S&P 500 Index near a record and the Dow having posted a new high last Monday.

Market summary

I hope you have a great week!

Warmest Regards,

Bill Stordahl, CFP®

Managing Director

Stordahl Capital Management

A Weekly Perspective on Planning and Markets

Each week, we share The Week in Review — a short collection of articles on

financial planning and wealth management, along with a brief overview for context.

One email per week. No promotions, no sales – just clarity.

Stordahl Capital Management, Inc is a Registered Investment Adviser. This commentary is solely for informational purposes and reflects the personal opinions, viewpoints, and analyses of Stordahl Capital Management, Inc. and should not be regarded as a description of advisory services or performance returns of any SCM Clients. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Advisory services are only offered to clients or prospective clients where Stordahl Capital Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Stordahl Capital Management unless a client service agreement is in place. Stordahl Capital Management, Inc provides links for your convenience to websites produced by other providers or industry-related material. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third-party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax, or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

1. The Dow Jones Industrials Average is an unmanaged index of 30 major companies which cannot be invested into directly. Past performance does not guarantee future results.

2. The NASDAQ Composite is an unmanaged index of companies which cannot be invested into directly. Past performance does not guarantee future results.

3. The S&P 500 Index is an unmanaged index of 500 larger companies which cannot be invested into directly. Past performance does not guarantee future results.

4. The Global Dow is an unmanaged index composed of stocks of 150 top companies. It cannot be invested into directly. Past performance does not guarantee future results.

5. CME Group front-month contract; Prices can and do vary; past performance does not guarantee future results.

6. CME Group continuous contract; Prices can and do vary; past performance does not guarantee future results.