How OPEC, Tariffs, and New Market Highs Shape the Case for Long-Term Investing

For most of the stock market's history, investing centered on selecting individual stocks and bonds.

Over recent decades, however, macroeconomic developments have come to play an increasingly significant role in shaping markets. Major events, whether tied to central bank decisions, geopolitical tensions, or shifts in global trade, now affect virtually all stocks regardless of company-specific fundamentals.

For investors, this shift means that constructing a modern portfolio is less about identifying attractive individual securities and more about making asset allocation decisions that align with long-term financial goals.

This dynamic has been especially evident over the past year and a half, during which two major macroeconomic forces have dominated: the war in Iran and U.S. tariff policy.

Although these are distinct developments, both influence consumer prices and business demand, whether directly through elevated energy costs or indirectly through the price of imported goods.

Importantly, the effects of macro-driven events like these tend to diminish over time. For this reason, investors are well served by keeping their focus on longer-term trends rather than reacting to any single event with portfolio changes.

The conflict in the Middle East, gasoline prices, and the shifting role of OPEC

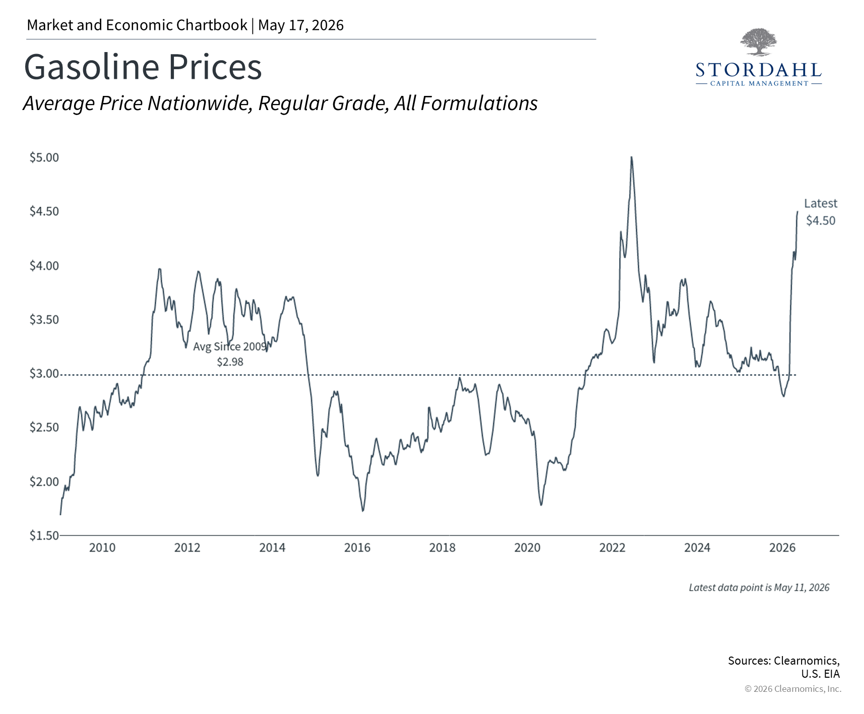

The most tangible way the conflict in Iran has reached American households is through rising fuel costs. The national average for regular unleaded gasoline has climbed to approximately $4.50 per gallon, well above the long-term average and a notable increase from levels seen just a few months prior. In certain regions of the country, prices have already surpassed $6 per gallon. (1) Because energy costs feed directly into the Consumer Price Index, headline inflation has moved higher, adding complexity to an economic environment that had been on an improving trajectory.

Some observers may find this environment reminiscent of the 1970s Arab Oil Embargo, when supply shocks drove inflation sharply higher and led to gasoline rationing. The world, however, has changed considerably since that era.

The United States is now the world's largest energy producer, outputting more than 13 million barrels of oil per day, which has significantly reduced the sensitivity of the U.S. economy to global oil disruptions.

Adding to this shift, the recent decision by the United Arab Emirates (UAE) to exit OPEC underscores how much the global energy landscape has evolved.

For decades, OPEC members played a central role in determining global oil prices by agreeing on production levels, a coordination challenge across roughly a dozen nations that has historically proved difficult to enforce. Preventing member countries from exceeding their agreed-upon production limits has been an ongoing source of friction within the group.

The UAE's departure reflects the diminishing cohesion of the cartel, as member nations increasingly pursue independent national strategies. At its peak during the 1970s, OPEC accounted for at least half of the world's oil supply.

Today, that share stands closer to one-third.(2) In response, the broader OPEC+ coalition, which includes Russia and other producers, was established, though the same coordination difficulties persist within that group as well.

The declining relevance of OPEC does not eliminate the risk of oil price spikes during periods of geopolitical stress, but it does mean that prices are less sensitive to OPEC's decisions than they once were.

While this offers little immediate relief to households managing higher fuel costs, it helps explain why the broader market impact of recent energy disruptions has been relatively contained.

Tariff policy faces ongoing legal challenges

The second major macroeconomic force shaping markets has been tariff policy, which continues to face significant legal scrutiny.

In February, the Supreme Court ruled that tariffs implemented last April under the International Emergency Economic Powers Act (IEEPA) are illegal. (3)

In response, the administration shifted to using Section 122 of the Trade Act of 1974 as the legal basis for these measures. More recently, the U.S. Court of International Trade ruled that these Section 122 tariffs are also unlawful. (4)

Despite these rulings, the administration has signaled its intent to continue pursuing tariffs as a central element of its geopolitical strategy.

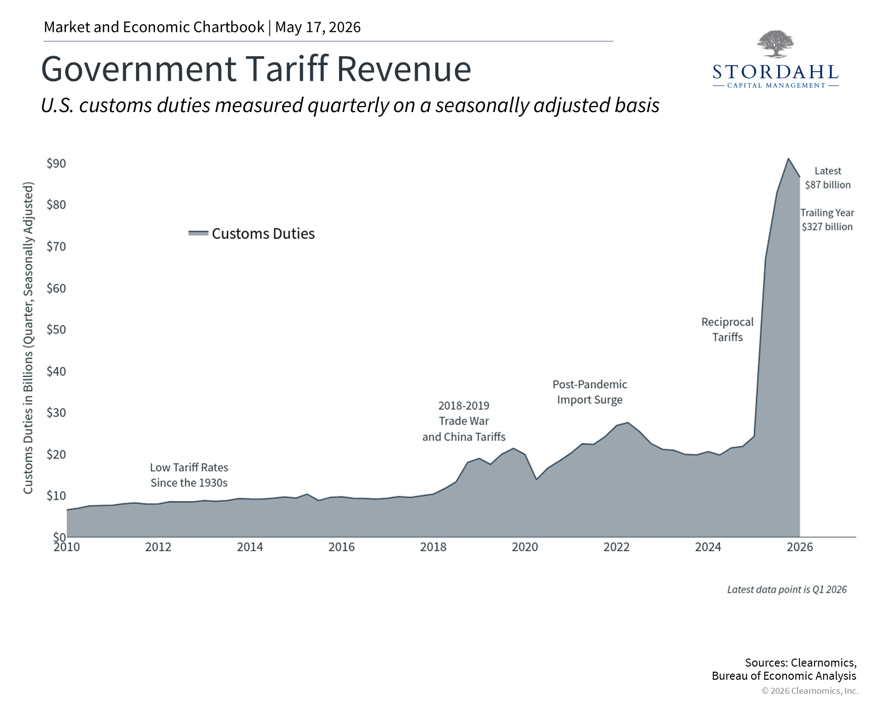

Other legal authorities remain available, including Section 301 of the Trade Act of 1974, which permits tariffs following formal investigations into specific countries' trade practices. Investigations of this kind have already been launched against dozens of countries, suggesting that tariffs will likely persist in some form, with country-specific rates becoming more prominent.

At the same time, the refund process for previously collected tariffs is now underway. Customs and Border Protection has begun processing refund claims, and some importers have already started receiving payments. (5) Estimates suggest that total refunds could reach between $160 and $170 billion.

The full scope and timeline of these refunds remains uncertain, but any amounts returned could provide a meaningful boost to earnings and cash flow for the importers that originally paid them.

From a purely economic standpoint, this represents a return of funds that were previously collected rather than a net new benefit. Even so, the refunds are a positive development for businesses and consumers alike.

Markets have pushed to new all-time highs even amid persistent uncertainty

For investors, the prevalence of global macro events means that broad market indices and individual stocks can move significantly based on factors unrelated to any specific company's operations or financial performance.

At the same time, one consistent characteristic of these events is that their market impact tends to diminish over time. Headlines surrounding wars, oil prices, tariffs, and similar issues can generate short-term volatility, but they rarely determine long-term investment outcomes.

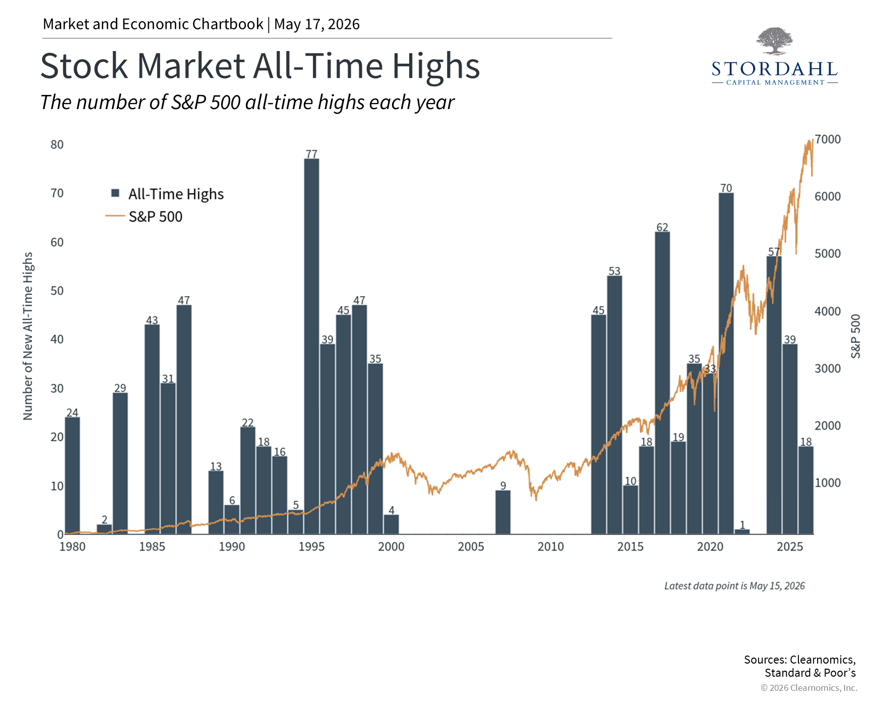

This is evident in the fact that, despite the considerable uncertainty of the past year and a half, the S&P 500 has still recorded more than a dozen new all-time highs this year.

As the accompanying chart illustrates, new all-time highs are a normal feature of bull markets, even as investor concerns remain a constant backdrop. What ultimately drives sustained market performance is the broader foundation of corporate earnings and economic growth, both of which have remained healthy throughout this period.

The bottom line? Today's market environment is shaped by global forces that tend to come and go. Staying invested with a well-constructed portfolio remains the best way to navigate uncertainty and achieve long-term financial goals.

Questions? We offer a complimentary 15-minute call to discuss your concerns and explore how we can assist you.

References

3. https://www.congress.gov/crs-product/LSB11398

4. https://www.cit.uscourts.gov/sites/cit/files/26-47.pdf

5. https://www.cbp.gov/trade/programs-administration/trade-remedies/ieepa-duty-refunds

Index Description

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

A Weekly Perspective on Planning and Markets

Each week, we share The Week in Review — a short collection of articles on

financial planning and wealth management, along with a brief overview for context.

One email per week. No promotions, no sales – just clarity.

Stordahl Capital Management, Inc is a Registered Investment Adviser. This commentary is solely for informational purposes and reflects the personal opinions, viewpoints, and analyses of Stordahl Capital Management, Inc. and should not be regarded as a description of advisory services or performance returns of any SCM Clients. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Advisory services are only offered to clients or prospective clients where Stordahl Capital Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Stordahl Capital Management unless a client service agreement is in place. Stordahl Capital Management, Inc provides links for your convenience to websites produced by other providers or industry-related material. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third-party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax, or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.